Perhaps you

might join me in wondering how sponsored researchers managed to convince FCC

Chairman Pai and others that network neutrality regulation singularly caused a near

immediate drop in infrastructure investment by U.S. carriers. How do you isolate the variable of “regulation”

from, for example, the investment cycle in migrating from 4G to next generation

5G wireless plan.

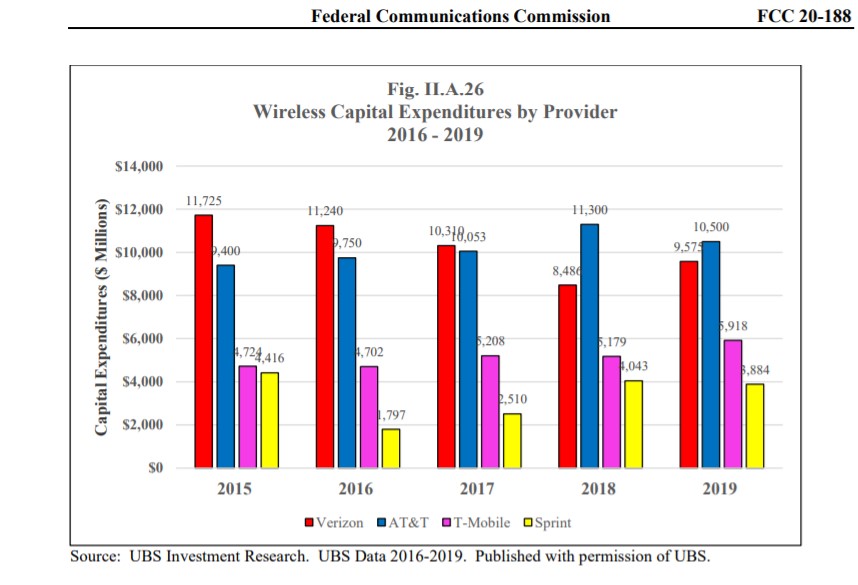

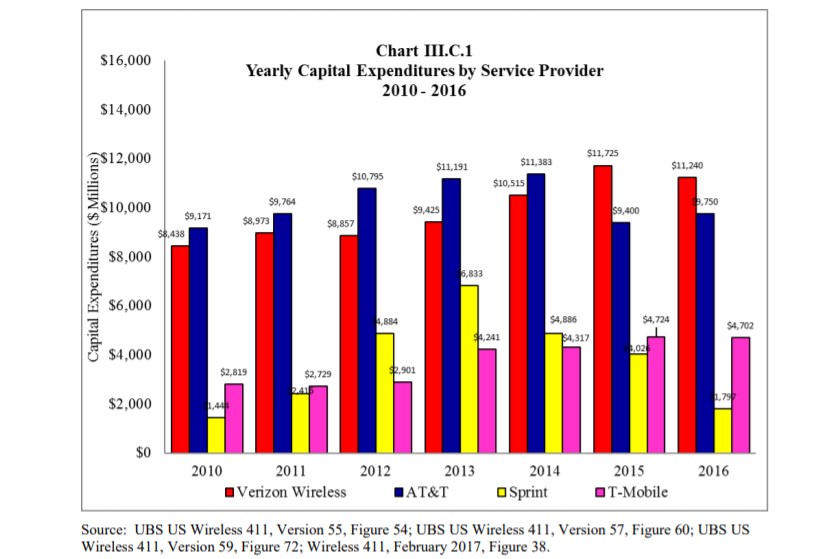

Set out

below, are two FCC charts that track capex incurred by the major U.S. wireless

carriers from 2010 to 2019:

S

S

Source: https://www.fcc.gov/20th-mobile-wireless-competition-report-quick-facts

From 2010

to 2019, the FCC toggled between imposing network neutrality requirements and

eliminating them. For purposes of our direct comparison of a regulatory or

deregulatory action and subsequent impact on investment, keep these years in

mind:

2010, the FCC approved the first

FCC Open Internet Order creating network neutrality rules and regulations; 2014,

the D.C. Circuit partially reverses the FCC on grounds that some of the network

neutrality requirements imposed common carrier duties on private, non-common

carriers; 2015, the FCC respond to the appellate court reversal with the

2015 Open Internet Order reclassifying broadband Internet as Title II regulated

common carrier telecommunications service; 2016, the D.C. Circuit defers

to the FCC and largely upholds the Commission; 2017-2018, the Ajit Pai

led FCC signals its priority in reversing the 2015 Open Internet Order and does

so in 2018 with the Restoring Internet Freedom Order.

Does

wireless carrier investment correlate up or down with the changing regulatory

regime? It sure does not look like it to me.

Even stakeholders, when communicating with buy side Wall Street analysts,

emphasize competitive necessity and the business cycle for next generation

network investment.

Regulation

does not matter significantly, until it becomes the sole predictor of

investment in a different forum.

S

S