With the FCC and most government actors obsessed with incentive creation, it makes sense to determine whether and how a regulatory or deregulatory action causes some desired outcome. Consider the creation of incentives to invest in physical plant. Incumbent carriers have spent a lot of time, money and effort arguing that regulation creates investment disincentives and deregulation does the desired opposite. This simplistic and not always correct premise constitutes the prevailing wisdom in the U.S.

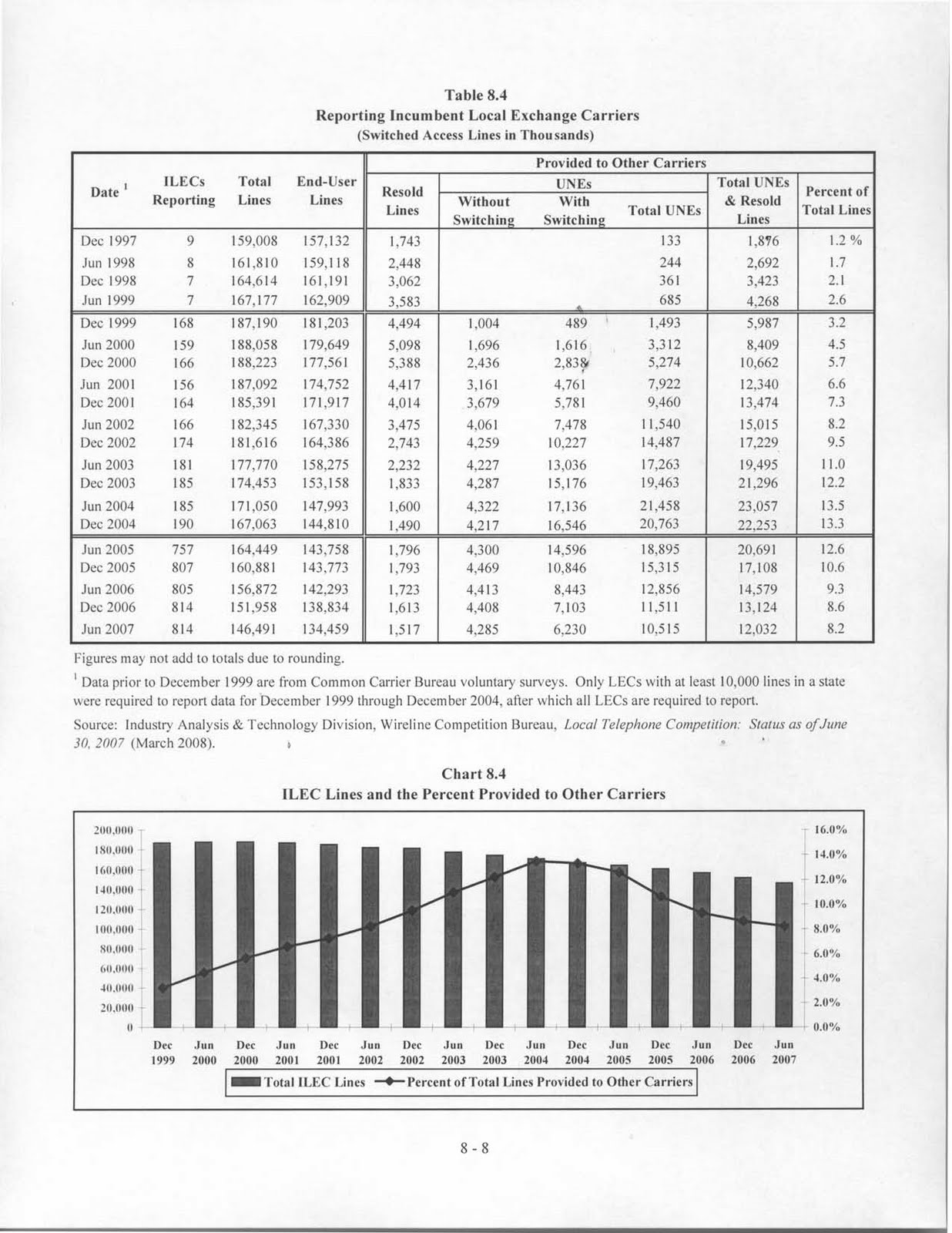

Using this mindset, sponsored researchers have argued that next generation network plant skyrocketed soon after the FCC abandoned local loop unbundling and other “sharing” requirements. Let’s probe this assertion. First, recall that local loop unbundling was not something incumbent Local Exchange Carriers (“ILECs”) gave away or shared. Resellers and repackagers of local switching and routing plant paid the incumbents, albeit at a rate below what the ILECs would like to have been paid. Second I have found—deep, deep, deep in the FCC’s obscure statistics and data collection process—that compulsory rentals from incumbents to newcomers peaked at 12%, a level never close to forcing incumbents to invest in plant that they would have to make available solely to competitors. See Trends in Telephone Service (Aug. 2008), at p. 8-8; available at http://hraunfoss.fcc.gov/edocs_public/attachmatch/DOC-284932A1.pdf.

The FCC stopped preparing this helpful source of information, but the percentage of resold ILEC lines has declined below the 8% reported in 2007 in light of the fact that rates to Competitive Local Exchange Carriers (“CLECs”) can exceed retail rates to end users, a price squeeze, but one the FCC and the Supreme Court in the Linkline case has no concerns.

Let’s assume that ILECs actually did increase their aggregate plant investment after the FCC abandoned local loop unbundling, bearing in mind that the Commission never required leasing of next generation plant such as dark or even lit fiber. Did deregulation cause all of the new investment? Of course not. Might the business cycle have had something to do with it? Might the cost of capital have had something to do with it? Might competitive necessity have had something to do with it? Oh and might declining market share and revenues in core business lines such as Plain Old Telephone Service have had something to do with it?

Whatever disincentive local loop unbundling imposed paled in comparison to incumbents’ need to find new revenues. Giving the ILECs due credit they have invested in next generation networks, mostly wireless and video plant for which no unbundling requirement ever applied. As to new found zeal in investing in Digital Subscriber Line services, might the ILECs want to make relatively small additional investment in already amortized copper plant, to secure some of the broadband growth market?

In a nutshell: do not buy the assertion that carriers make investment go/no decisions solely on the state of regulatory oversight. Carriers make sound business decisions, affected more by business conditions than the relatively minor impact of any FCC regulatory or deregulatory decision.

Using this mindset, sponsored researchers have argued that next generation network plant skyrocketed soon after the FCC abandoned local loop unbundling and other “sharing” requirements. Let’s probe this assertion. First, recall that local loop unbundling was not something incumbent Local Exchange Carriers (“ILECs”) gave away or shared. Resellers and repackagers of local switching and routing plant paid the incumbents, albeit at a rate below what the ILECs would like to have been paid. Second I have found—deep, deep, deep in the FCC’s obscure statistics and data collection process—that compulsory rentals from incumbents to newcomers peaked at 12%, a level never close to forcing incumbents to invest in plant that they would have to make available solely to competitors. See Trends in Telephone Service (Aug. 2008), at p. 8-8; available at http://hraunfoss.fcc.gov/edocs_public/attachmatch/DOC-284932A1.pdf.

The FCC stopped preparing this helpful source of information, but the percentage of resold ILEC lines has declined below the 8% reported in 2007 in light of the fact that rates to Competitive Local Exchange Carriers (“CLECs”) can exceed retail rates to end users, a price squeeze, but one the FCC and the Supreme Court in the Linkline case has no concerns.

Let’s assume that ILECs actually did increase their aggregate plant investment after the FCC abandoned local loop unbundling, bearing in mind that the Commission never required leasing of next generation plant such as dark or even lit fiber. Did deregulation cause all of the new investment? Of course not. Might the business cycle have had something to do with it? Might the cost of capital have had something to do with it? Might competitive necessity have had something to do with it? Oh and might declining market share and revenues in core business lines such as Plain Old Telephone Service have had something to do with it?

Whatever disincentive local loop unbundling imposed paled in comparison to incumbents’ need to find new revenues. Giving the ILECs due credit they have invested in next generation networks, mostly wireless and video plant for which no unbundling requirement ever applied. As to new found zeal in investing in Digital Subscriber Line services, might the ILECs want to make relatively small additional investment in already amortized copper plant, to secure some of the broadband growth market?

In a nutshell: do not buy the assertion that carriers make investment go/no decisions solely on the state of regulatory oversight. Carriers make sound business decisions, affected more by business conditions than the relatively minor impact of any FCC regulatory or deregulatory decision.